Every public company in the United States talks to its investors through a fixed vocabulary of forms. The SEC’s EDGAR system holds millions of them, and almost everything you’d want to know about a public company — what it earns, who runs it, who owns it, what it just agreed to do — lives inside one of about a dozen form types.

The hard part isn’t finding the forms. It’s knowing which one answers your question. This guide is the map: each major filing type, who files it, how often, and the one thing you’d actually open it for. Where a form deserves its own deep dive, we link to it.

The periodic reports — what a company earns and how it’s doing

These three are the backbone. Every operating company files them on a schedule, and together they cover the financial story.

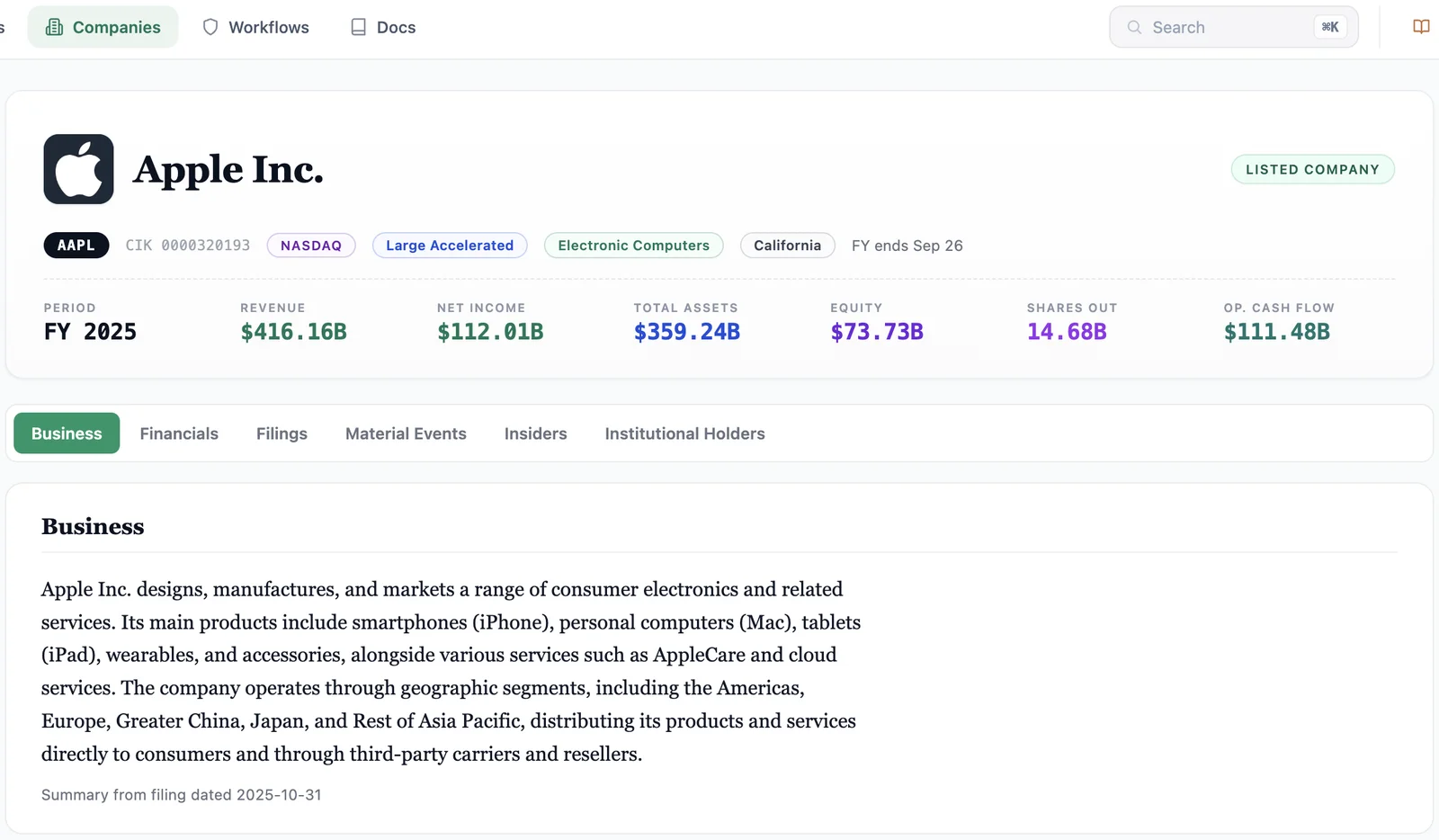

10-K — the annual report. Filed once a year, within 60–90 days of fiscal year-end (the window depends on company size). This is the comprehensive one: audited financial statements, the full business description, the risk factors, and Management’s Discussion and Analysis (MD&A) of results. If you read one filing on a company, read the 10-K. (A dedicated “how to read a 10-K” walkthrough is coming next in this series.)

10-Q — the quarterly report. Filed for each of the first three fiscal quarters (the fourth is folded into the 10-K), within 40–45 days of quarter-end. Lighter than the 10-K and unaudited, but it’s where you catch a trend changing direction a quarter before the annual report confirms it.

8-K — the current report. Filed within four business days of a specific triggering event — an acquisition, an executive departure, a new credit facility, an earnings release, a material impairment. The 8-K is event-driven, not scheduled, so it’s the form that tells you something happened now. There are roughly 30 distinct things that trigger one, each with its own item number. → The 8-K item index decodes every item number from 1.01 to 9.01.

Read it for the full picture

- 10-K — once a year, audited, comprehensive

- 10-Q — quarterly, unaudited, trend-catching

Read it for what just happened

- 8-K — within 4 business days of an event

- Item-coded so you can filter to the events that matter

The ownership filings — who holds the shares

Three families of form disclose who owns what, and they answer different questions.

Forms 3, 4, and 5 — insider transactions. Officers, directors, and 10%+ owners file these. Form 3 is the initial statement of holdings; Form 4 reports each transaction within two business days (the one most people watch — it’s how you see an insider buying or selling on the open market); Form 5 is an annual catch-up. The signal is in the transaction code: an open-market purchase (code P) reads very differently from a tax-withholding sale on vested stock. (A “Form 4 explained” deep dive on the transaction codes is coming in this series.)

Schedules 13D and 13G — large beneficial owners. Anyone crossing 5% ownership of a public company files one of these. 13D is the activist version — it signals intent to influence control and comes with a far tighter deadline. 13G is the passive version for institutions and long-term holders. The 2024 amendments shortened both deadlines significantly. → Schedule 13D vs 13G explained covers the threshold, the intent test, and the new deadlines.

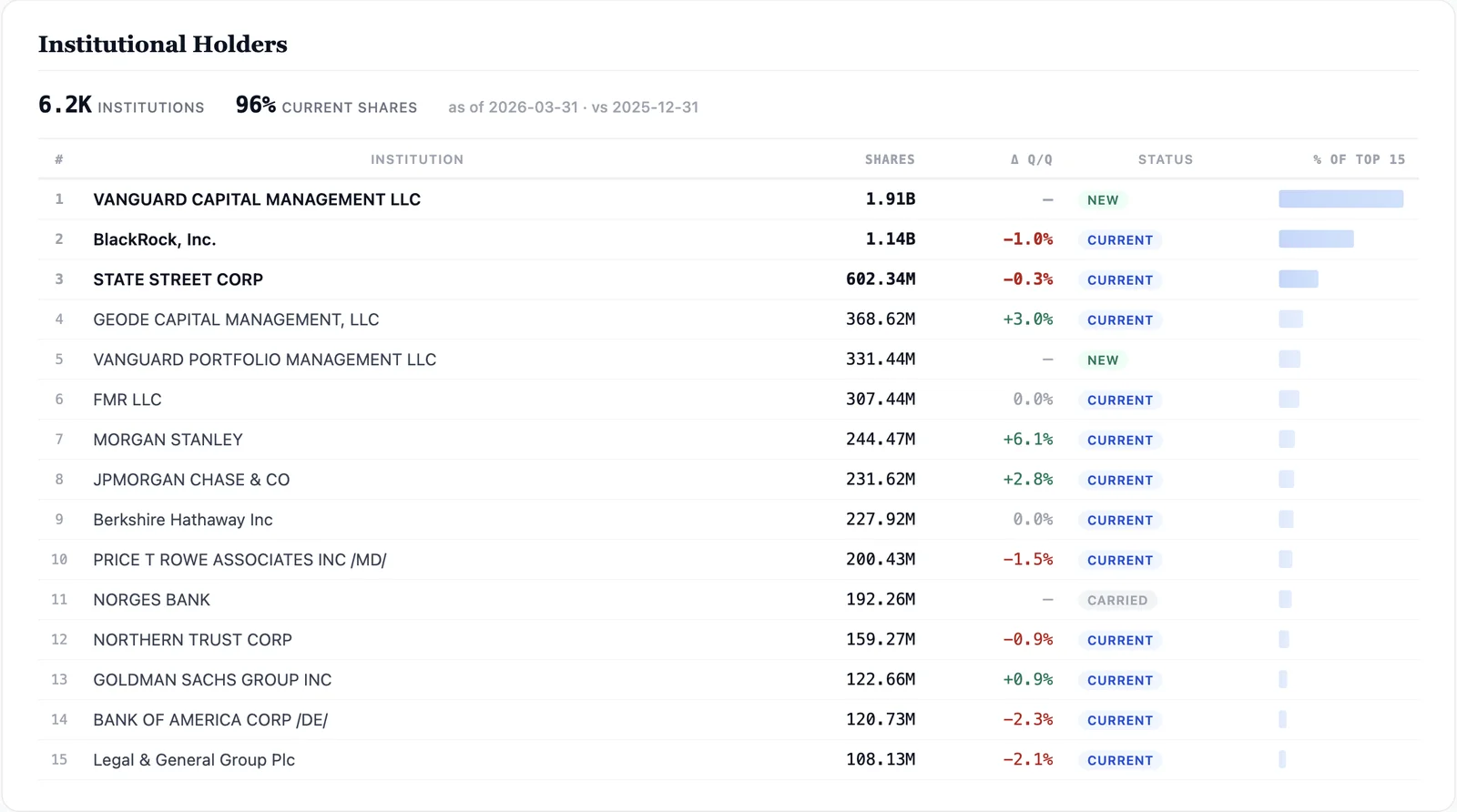

Form 13F — institutional holdings. Investment managers with over $100 million in qualifying assets file a quarterly snapshot of their U.S. equity positions, due 45 days after quarter-end. It’s how you see what Berkshire, Baillie Gifford, or a hedge fund held as of the report date — with the standard caveat that it’s a 45-day-stale, long-only-ish snapshot.

The offering documents — when a company raises money

S-1 — the IPO registration. A company going public files an S-1 to register its shares. It’s the first comprehensive public disclosure a private company makes, and it reads like a 10-K written by a company that has never had to talk to public investors before — dense, revealing, and worth reading in full for a name you’re underwriting.

424B (B1 through B8) — the prospectus. Once a registration is effective, the actual offering terms — price, size, underwriters, use of proceeds, dilution — land in a 424B prospectus. The suffix tells you the offering type. These are where the real economics of a raise are disclosed.

S-3 — the shelf registration. A streamlined registration available to established companies, letting them register securities now and sell them later (“off the shelf”) via a short prospectus supplement. A shelf doesn’t mean a sale is imminent — it means the company has loaded the gun.

The governance and fund filings

DEF 14A — the proxy statement. Filed ahead of the annual meeting, this is where executive compensation, board nominees, and shareholder proposals get disclosed. If you want to know what the CEO is actually paid — all-in, with the perks — the proxy is the source, not the 10-K.

Form ADV — investment adviser registration. Registered investment advisers file Form ADV to disclose their business, assets under management, conflicts, and disciplinary history. Part 2 is the plain-English brochure clients receive.

N-PORT and N-CEN — fund holdings and operations. Registered funds (mutual funds, ETFs) report portfolio holdings monthly (N-PORT) and operational details annually (N-CEN). This is the fund-world analogue to a 13F.

How the forms connect

The forms aren’t islands. An 8-K Item 1.01 announcing a merger agreement points forward to the 8-K Item 2.01 that reports the closing, the S-4 that registers the deal shares, and the 13D an arbitrageur files when they cross 5% of the target. A 10-K’s risk-factor section is best read as a diff against last year’s. Reading SEC filings well is mostly about knowing which form answers the question in front of you — and following the thread between them.

That threading is exactly what edgar.tools is built to do: resolve a company once, then move between its filings, its ownership, and its disclosures without re-finding it on EDGAR each time. You can do it on the company page or hand the whole surface to an AI assistant through the MCP server.

Read any company’s filings for free — no card required. Start at app.edgar.tools.