A Form 25-NSE hits the EDGAR tape and the headline writes itself: “[Company] delisted.” It sounds terminal. Often it isn’t. The same form is filed when a bond matures on schedule, when a merger closes, and when an exchange finally strikes a company that can’t meet its listing standards — three completely different stories wearing one filing code.

The good news: the filing tells you which story you’re looking at, in a single line. You just have to know where to look. This post is the decoder — and an original count of where a full year of these filings actually land.

A note on method: the breakdown below comes from running every Form 25-NSE filed in the 12 months through June 2026 — 917 filings — through the same §240.12d2-2 rule classifier edgar.tools uses on the live tape. Counts are mine; the rule semantics are the SEC’s.

What is a Form 25-NSE?

Form 25 — officially “Notification of Removal from Listing and/or Registration under Section 12(b) of the Securities Exchange Act of 1934” — is the document that removes a security from a national exchange. It’s filed electronically on EDGAR as a 25-NSE under SEC Rule 12d2-2. (Form 25 itself is a one-pager.)

Here’s the first surprise: the exchange files it, not the company. When Nasdaq or the NYSE removes a security, the exchange is the filer and the company is the “subject.” That’s why a delisting can show up on EDGAR under “Nasdaq Stock Market LLC” rather than the company you’re searching for — and why the same filing often appears twice, cross-indexed under both the exchange and the issuer.

Across the year, the filings split by venue almost exactly the way listings do: Nasdaq 47%, NYSE 38%, with NYSE Arca, Cboe BZX, and NYSE American making up the rest.

The one line that matters: the rule provision

Every 25-NSE cites the specific paragraph of Rule 12d2-2 it rests on — something like 17 CFR 240.12d2-2(a)(1) or (b). That citation looks like legal boilerplate. It’s actually the whole story. Read the letter in the parentheses first:

| Rule cited | What it means | What it signals |

|---|---|---|

| (a)(1) / (a)(2) | The entire class was called, redeemed, or reached maturity — almost always a bond or note ending its life | Routine. Nothing happened to the company. |

| (a)(3) | Securities converted “by operation of law or otherwise” — typically a merger closing or a go-private deal | Usually benign. The company was acquired or taken private. |

| (a)(4) | All rights in the class were extinguished | Rare, routine. |

| (b) | The exchange removed the security because it no longer meets continued-listing standards | Distress. This is the one to read closely. |

| (c) | The issuer voluntarily withdrew from listing | Voluntary. |

| (d) | Procedural / timing provisions | Procedural. |

Paragraph (a) is mandatory and mechanical — the class of securities simply stopped existing. Paragraph (b) is discretionary: the exchange chose to pull the security because the issuer failed a continued-listing rule (minimum bid price, market cap, shareholder count, late filings). That single letter — (a) versus (b) — is the difference between “a note matured” and “a company is in trouble.”

Where a year of delistings actually land

When you decode all 917 filings, the “delisting = failure” narrative falls apart:

Routine — about 85%

- (a)(3) mergers & conversions — 46%. A deal closed; the shares became something else.

- (a)(1)/(a)(2) redemptions & maturities — 38%. Mostly banks’ notes and structured products reaching the end of their term. High volume, zero drama.

Distress — about 15%

- (b) exchange-initiated — 15% (139 filings). The exchange struck the security for failing listing standards. This is the only bucket that means what the headline implies.

The redemption pile is the quiet giant: a huge share of all 25-NSEs are routine note and ETN expirations from the likes of bank issuers — they dominate the raw count and almost never matter to anyone but the holders. Meanwhile the distress (b) filings skew heavily toward micro-cap biotech, foreign small-caps, and post-deal SPACs — with the occasional real operating company in the mix (over the year: ModivCare, Spirit Aviation Holdings, Cumulus Media, TPI Composites, Cutera).

The two clocks: delisting vs. deregistration

A 25-NSE starts two timers that people routinely conflate.

- Trading stops in 10 days. Removal from the exchange takes effect 10 days after the Form 25 is filed. The stock is no longer “listed.”

- Registration ends in 90 days. Termination of the Section 12(b) registration takes effect 90 days after filing (or sooner if the SEC allows). During that window, the company still owes any periodic reports that come due.

And a third, often-missed step: delisting is not the same as going dark. A company large enough to be registered under Section 12(g) keeps its reporting obligations even after it leaves the exchange. To actually stop filing 10-Ks and 10-Qs, it has to file a separate Form 15 — which it can only do once its shareholder count drops low enough (broadly, under 300 holders of record, or under 500 with less than $10M in assets). Plenty of delisted companies keep reporting for years.

What happens to your shares

When a stock is involuntarily delisted, it doesn’t vanish — it moves down-market, usually to the OTC markets (the Pink or Grey tiers), where disclosure is thin. Two things tend to follow:

- Quotes can freeze. If the company stops filing public reports, SEC Rule 15c2-11 can prevent broker-dealers from publishing quotes — which makes the shares genuinely hard to sell through a normal brokerage account.

- Forced selling accelerates the slide. Many funds have charter rules against holding unlisted securities, so a delisting triggers mechanical selling on top of whatever caused the trouble.

For tax purposes, delisting by itself isn’t a taxable event — a loss is realized only when you sell or the shares are proven worthless.

The same form, two opposite stories

Two 25-NSEs from the past year, side by side:

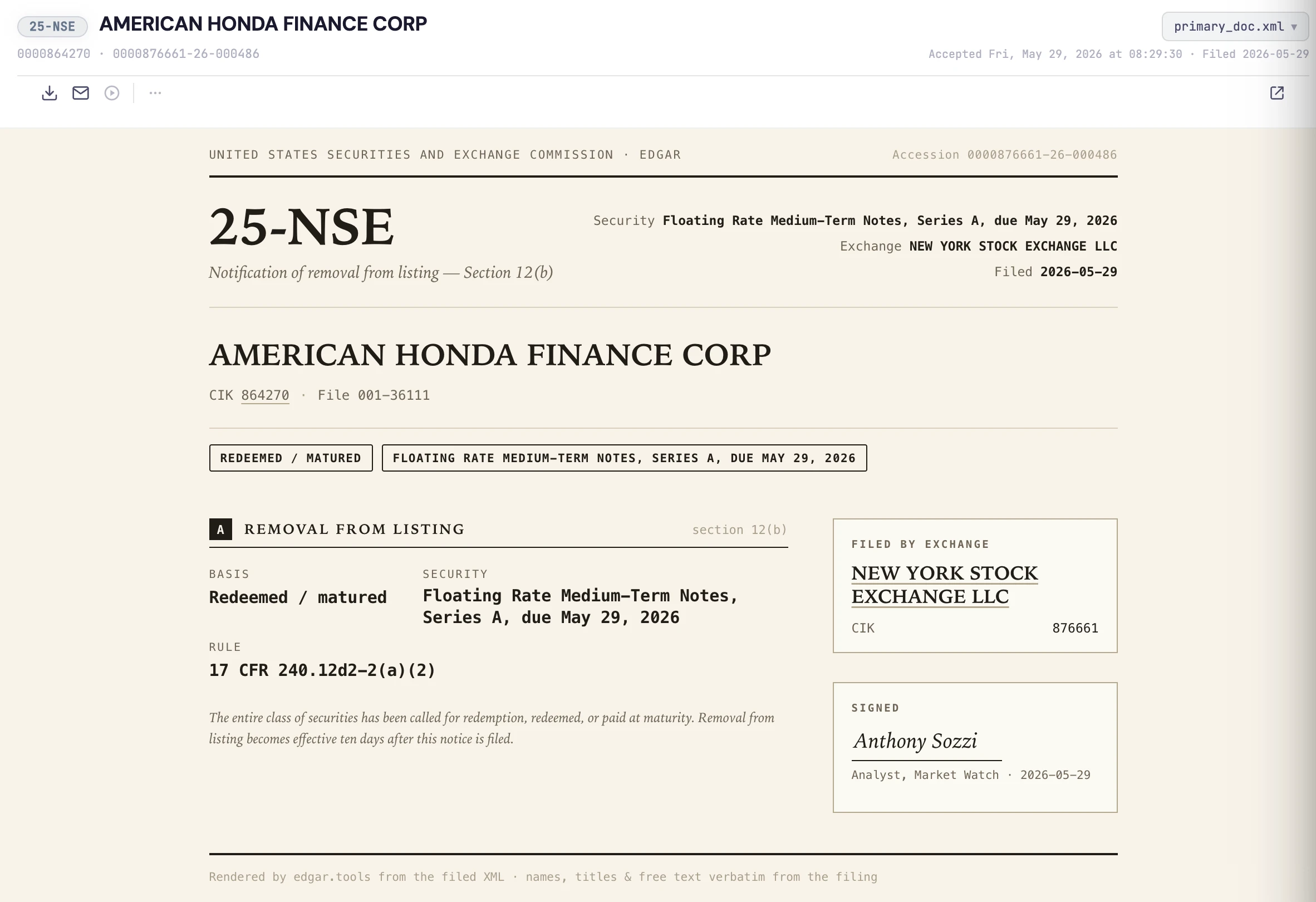

- American Honda Finance Corp files a 25-NSE under (a)(2) when its Floating Rate Medium-Term Notes, Series A, due May 2026 reach maturity. Routine. The issuer is as healthy as ever; a bond simply reached the finish line.

- Luminar Technologies is removed by Nasdaq after its Chapter 11 — the (b) distress case, the shares dropping to OTC as LAZRQ. The warning, as it happens, was sitting in the 8-K tape six weeks earlier: see the full forensic walkthrough in What you could have known on October 31.

Same filing code. One is paperwork; the other is an obituary. The rule provision is what tells them apart.

Reading delistings on edgar.tools

edgar.tools does this decode for you. Every 25-NSE on the tape gets its rule provision parsed into plain language — redemption, merger conversion, or exchange-initiated distress — and the page leads with the delisted company, not the exchange that filed it, so you’re not hunting through “Nasdaq Stock Market LLC” to find the name you care about.

17 CFR 240.12d2-2(a)(2) becomes a Redeemed / matured badge, the company leads, and the exchange that actually filed it (NYSE) drops to a side card. A note reached maturity — routine, and labeled as such.In the news feed, the routine redemptions like this one are damped and only the rare distress delistings surface.

If you want to catch a specific name the day it’s struck, a Sentinel can watch delisting activity across a watchlist or peer set and deliver an AI-analyzed brief — distress flagged, paperwork ignored.

New to SEC forms? Start with the SEC filing types guide, or track filings free at app.edgar.tools — no card required.